Share:

Blog

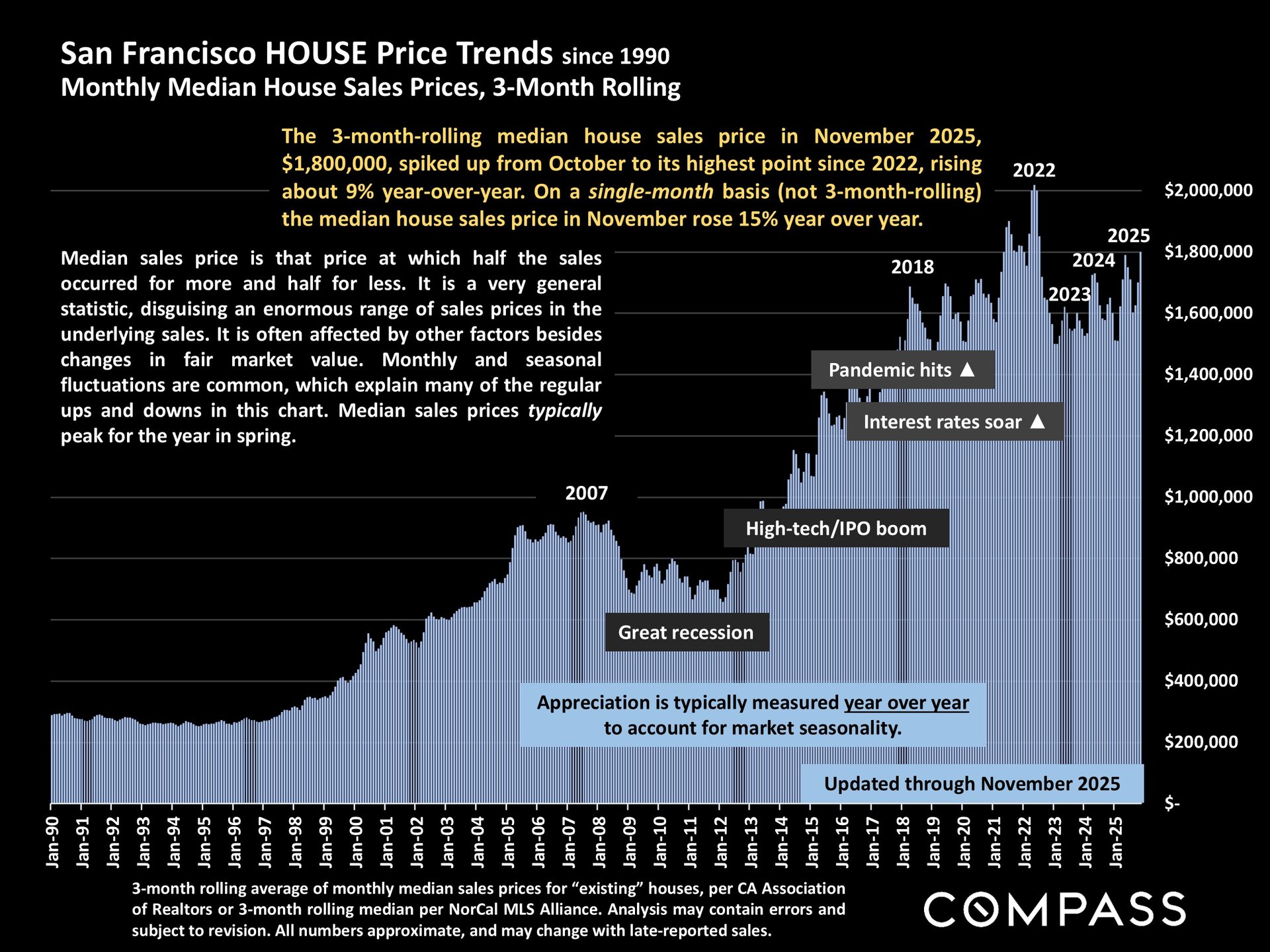

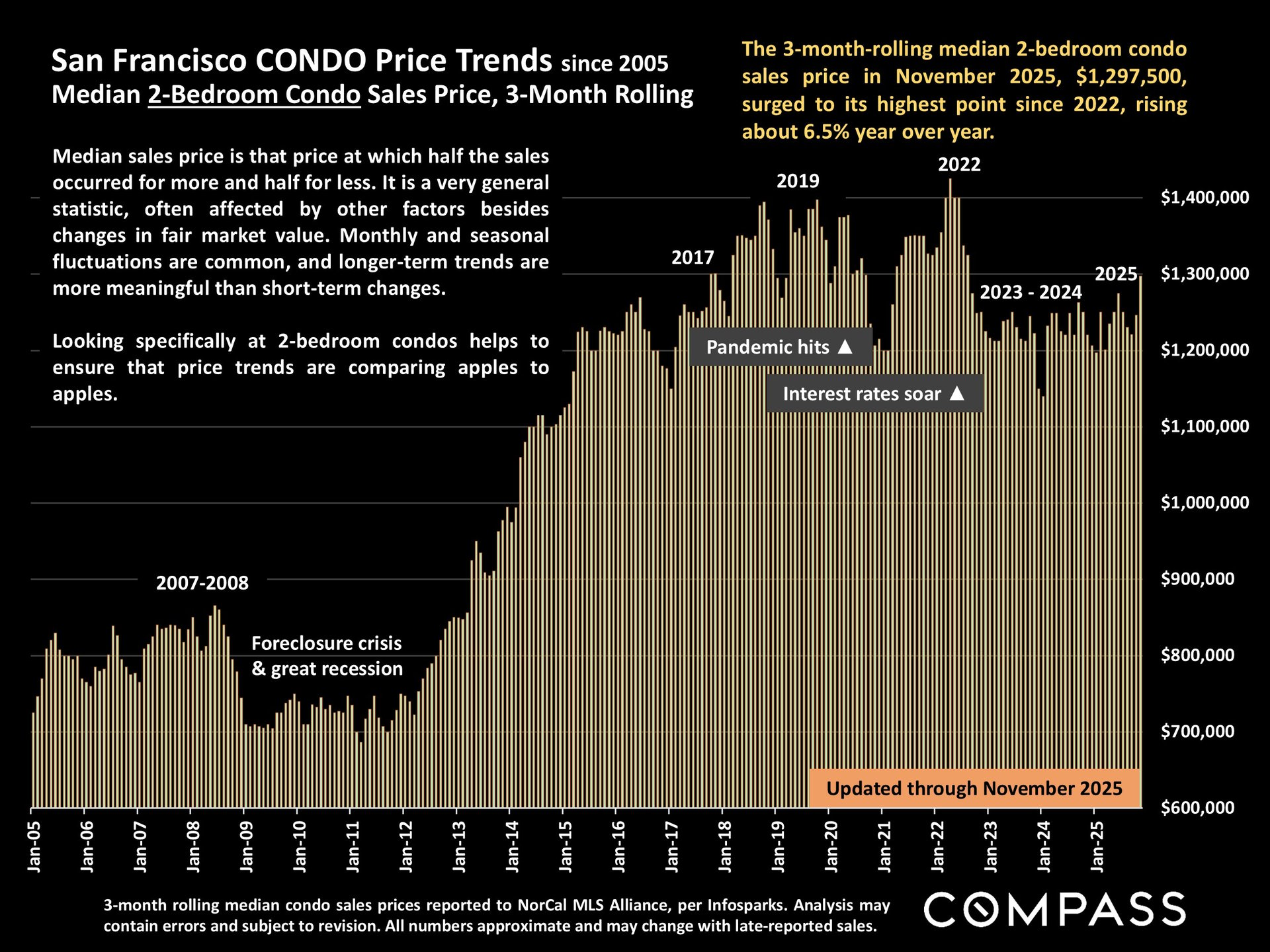

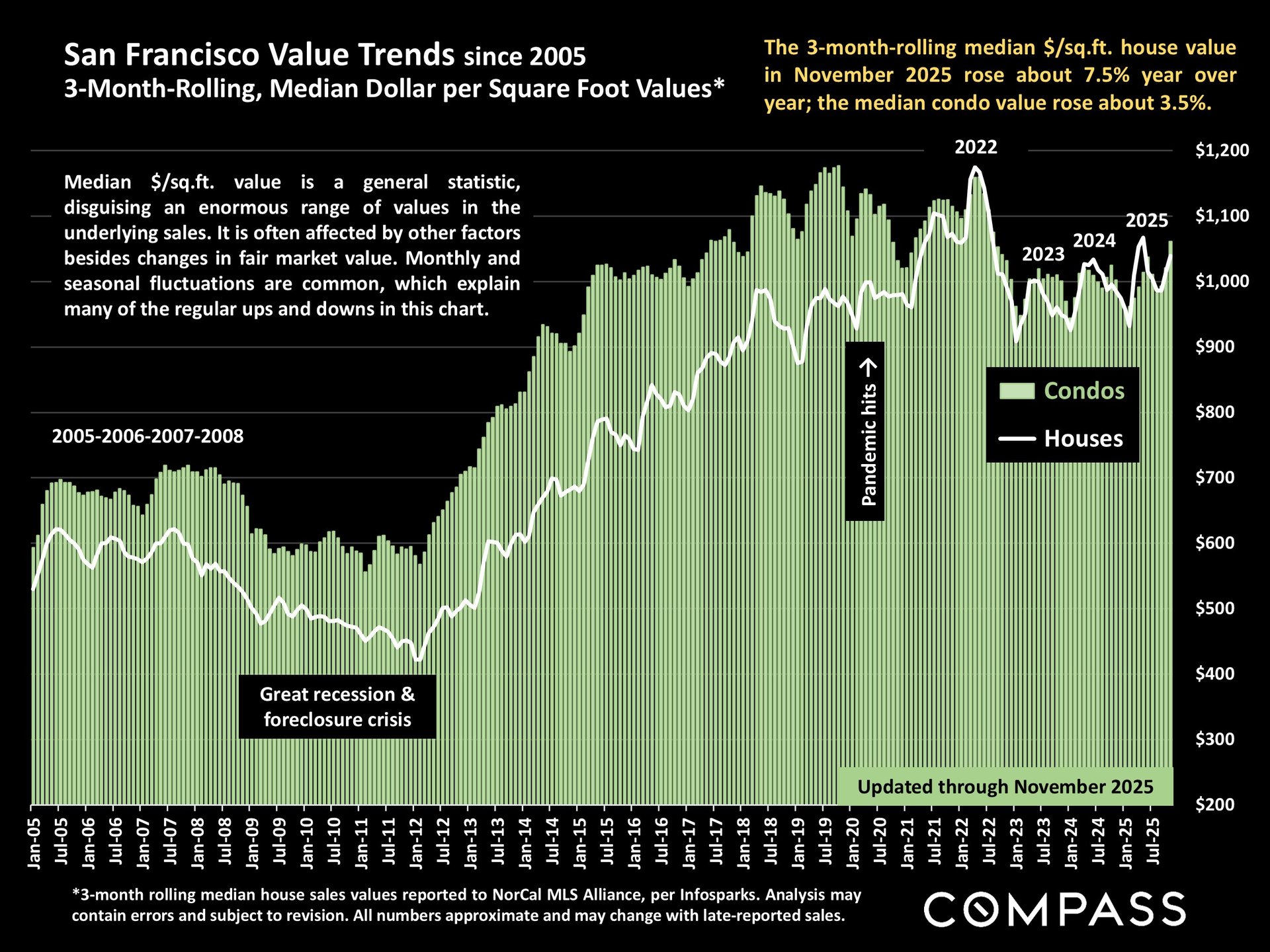

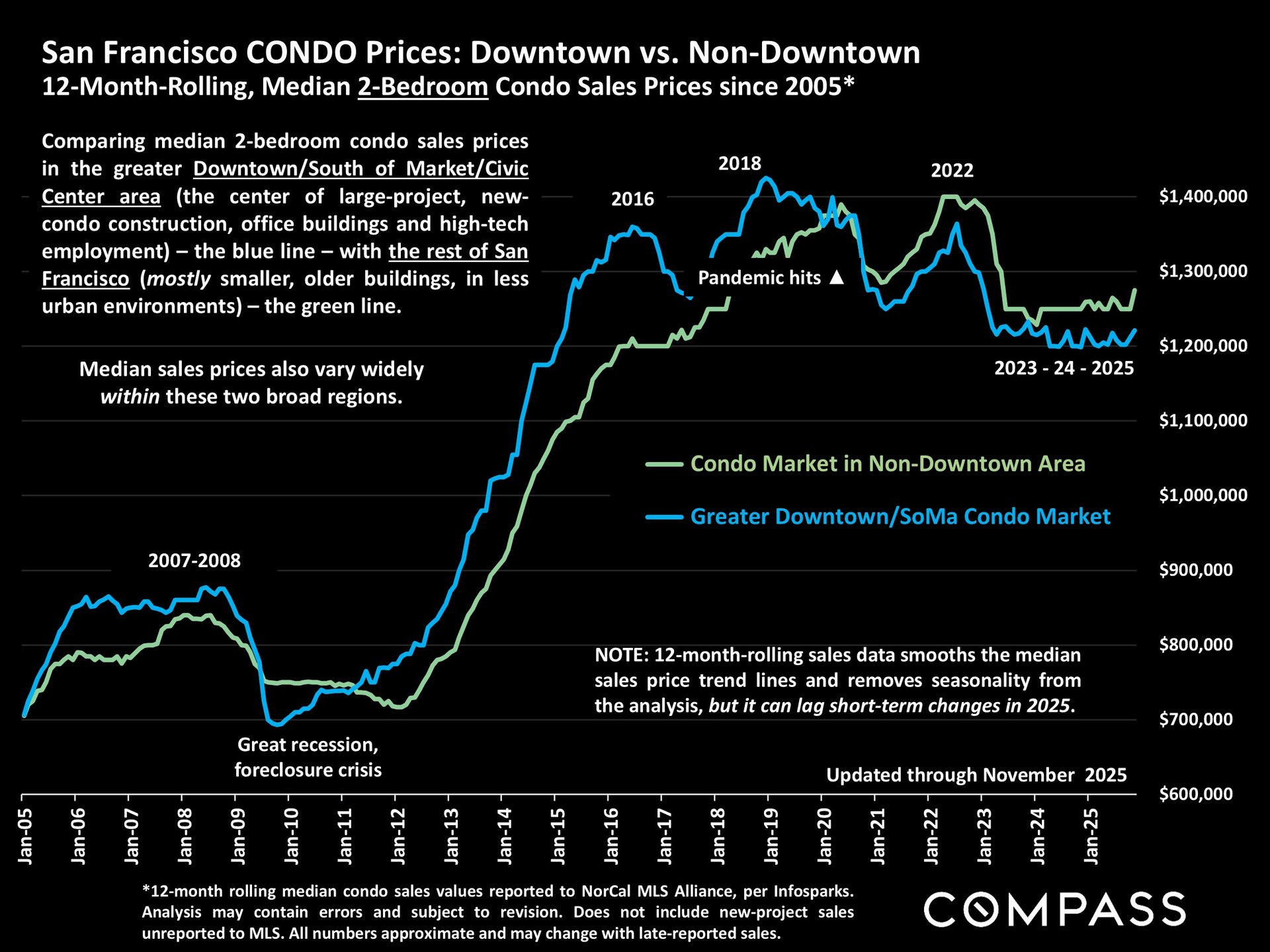

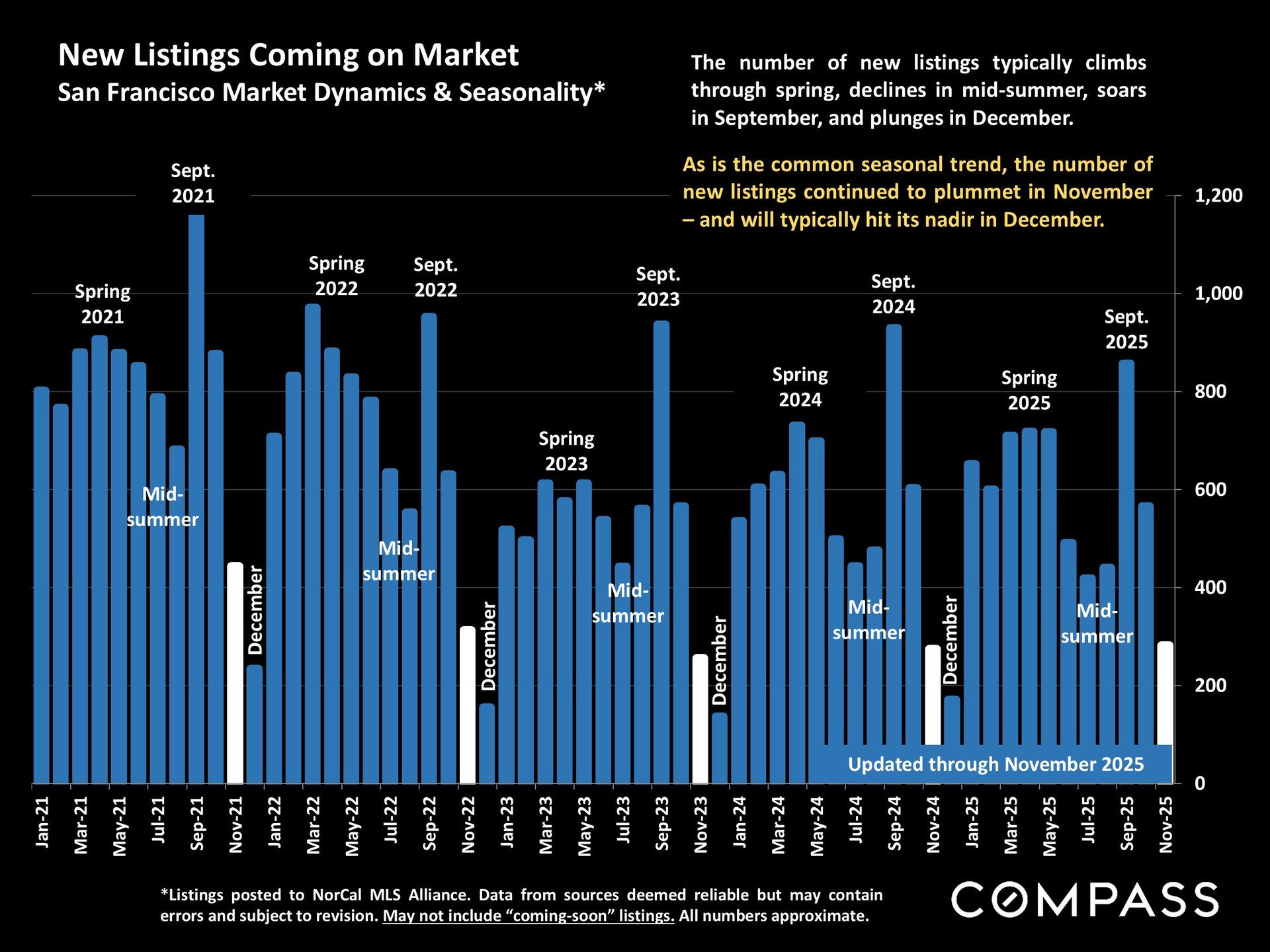

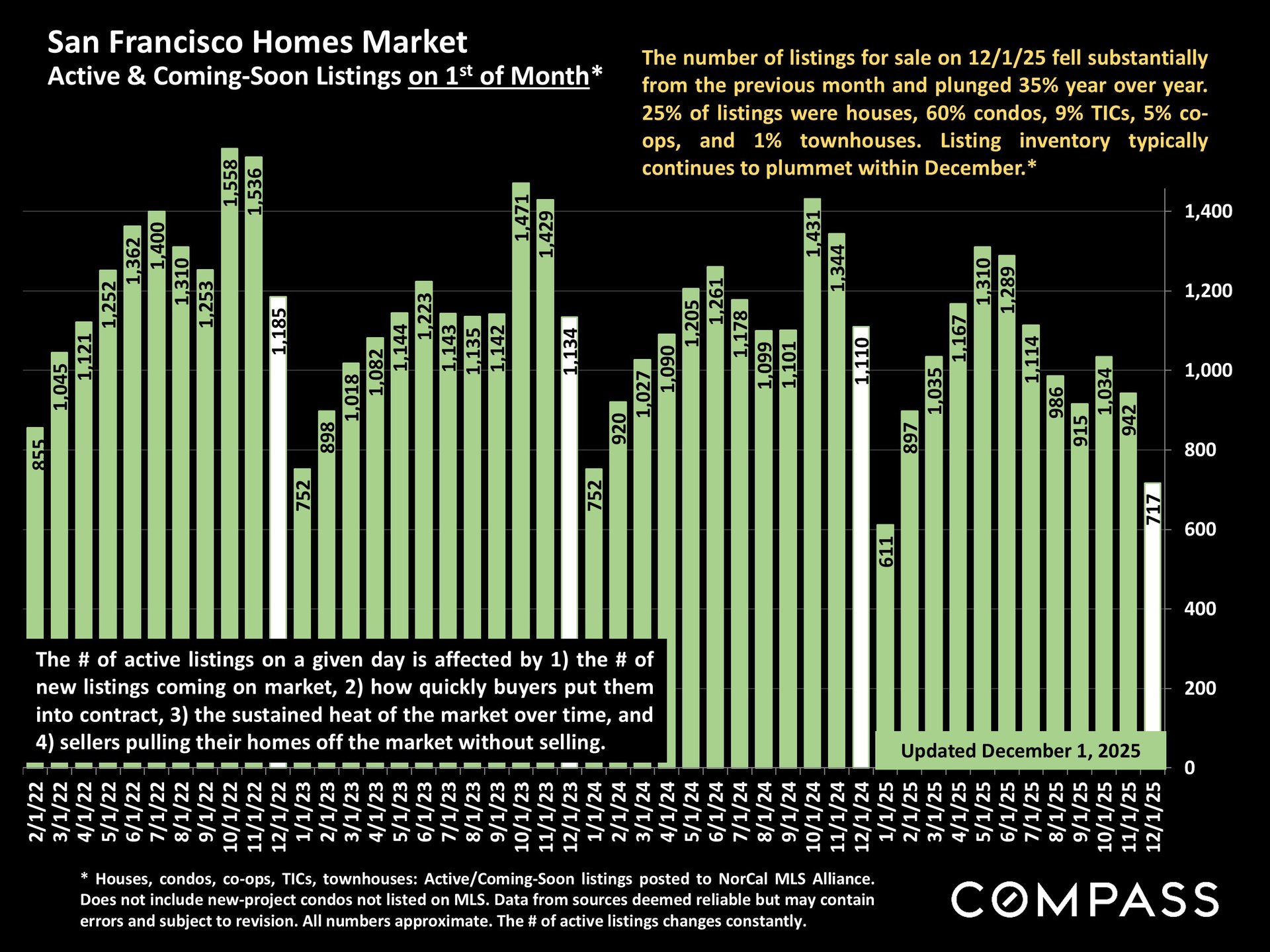

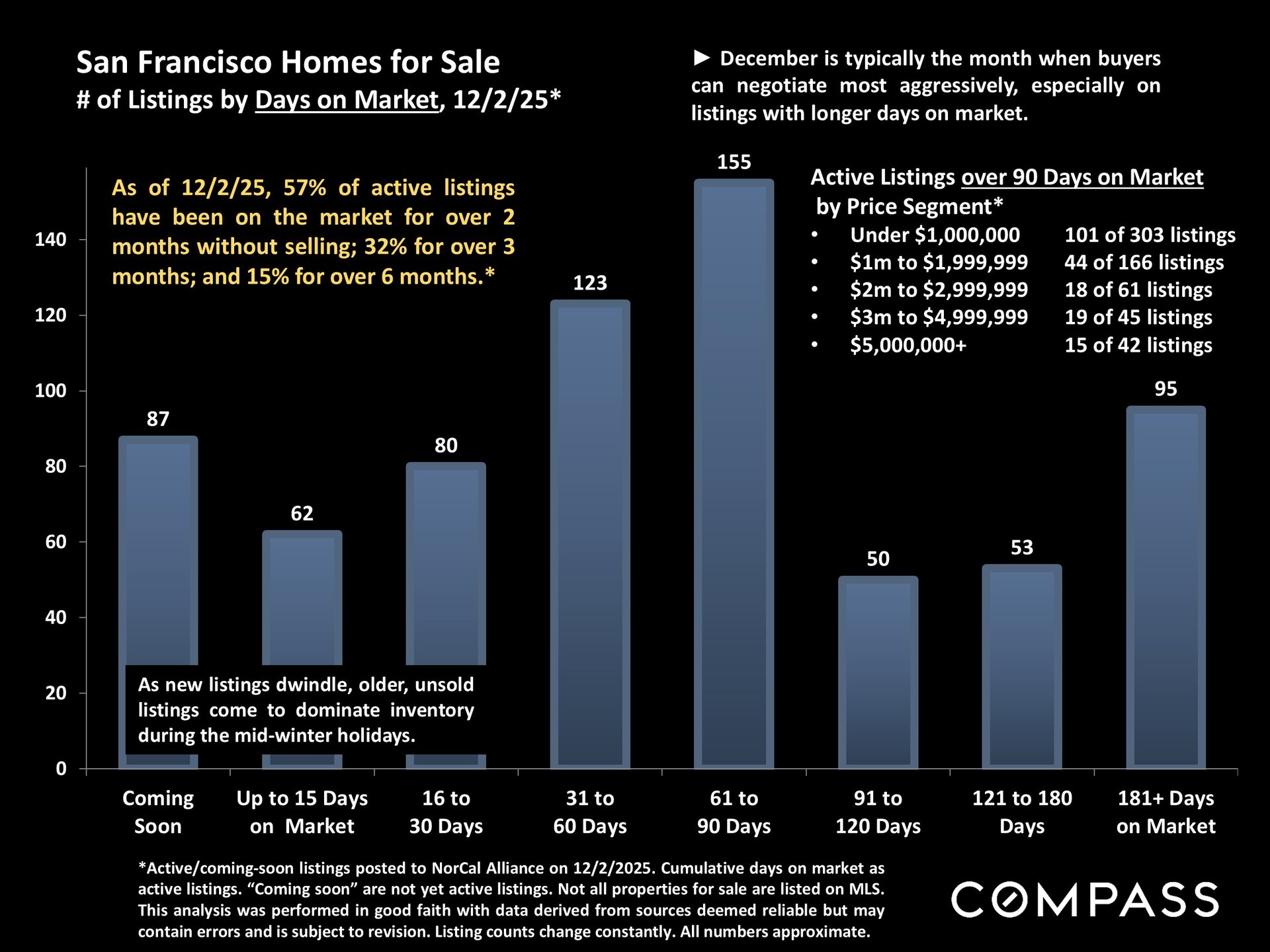

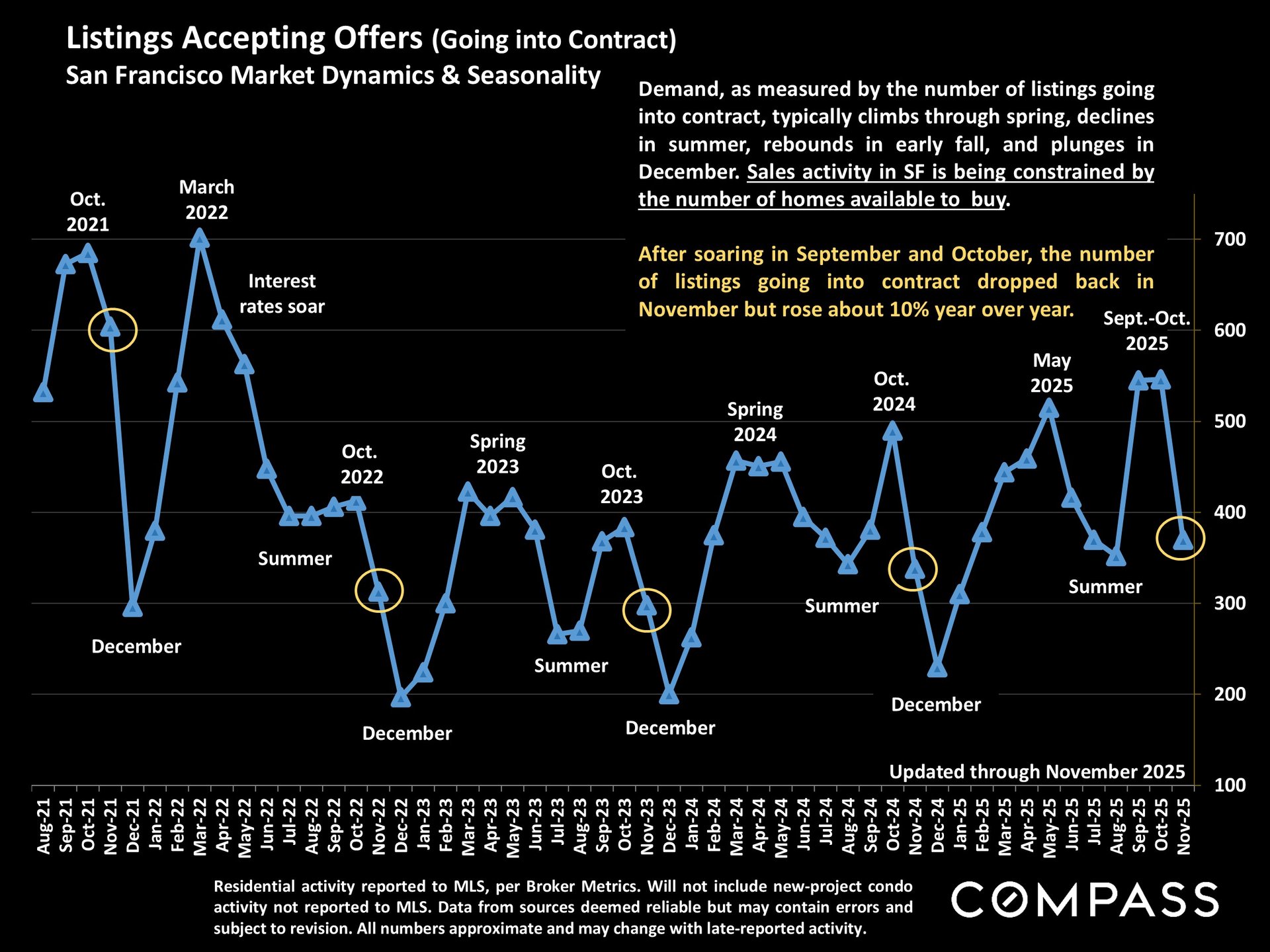

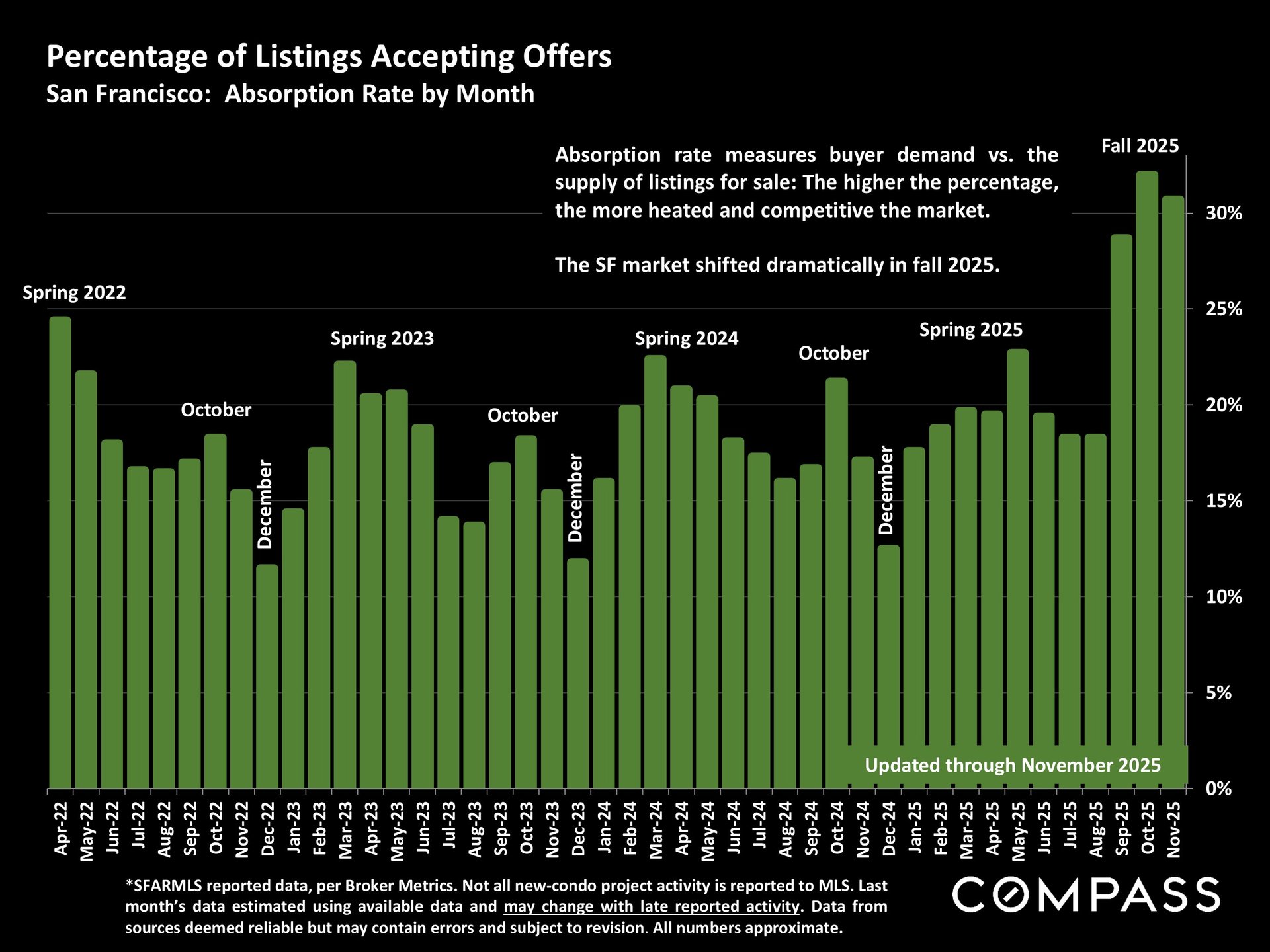

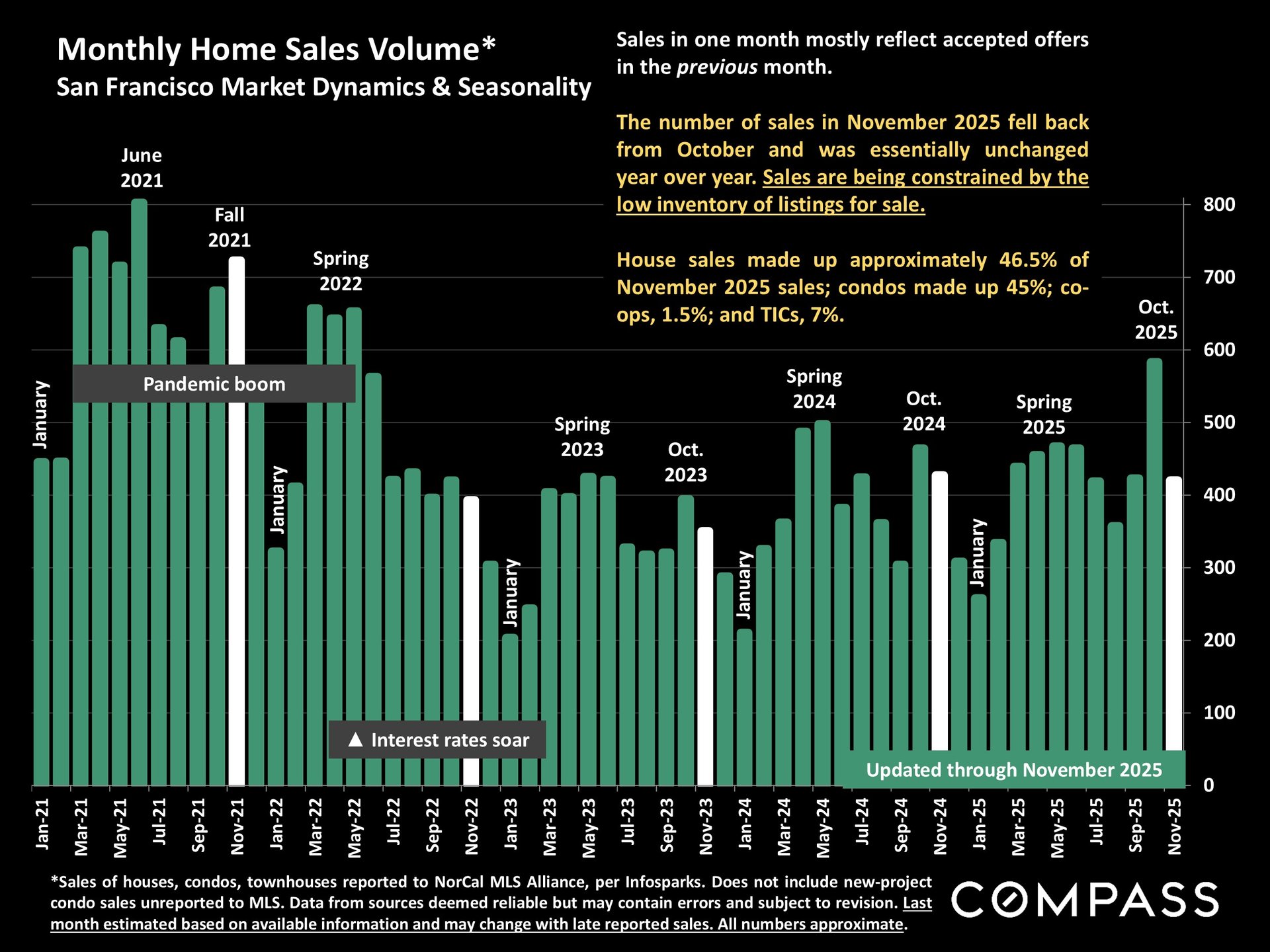

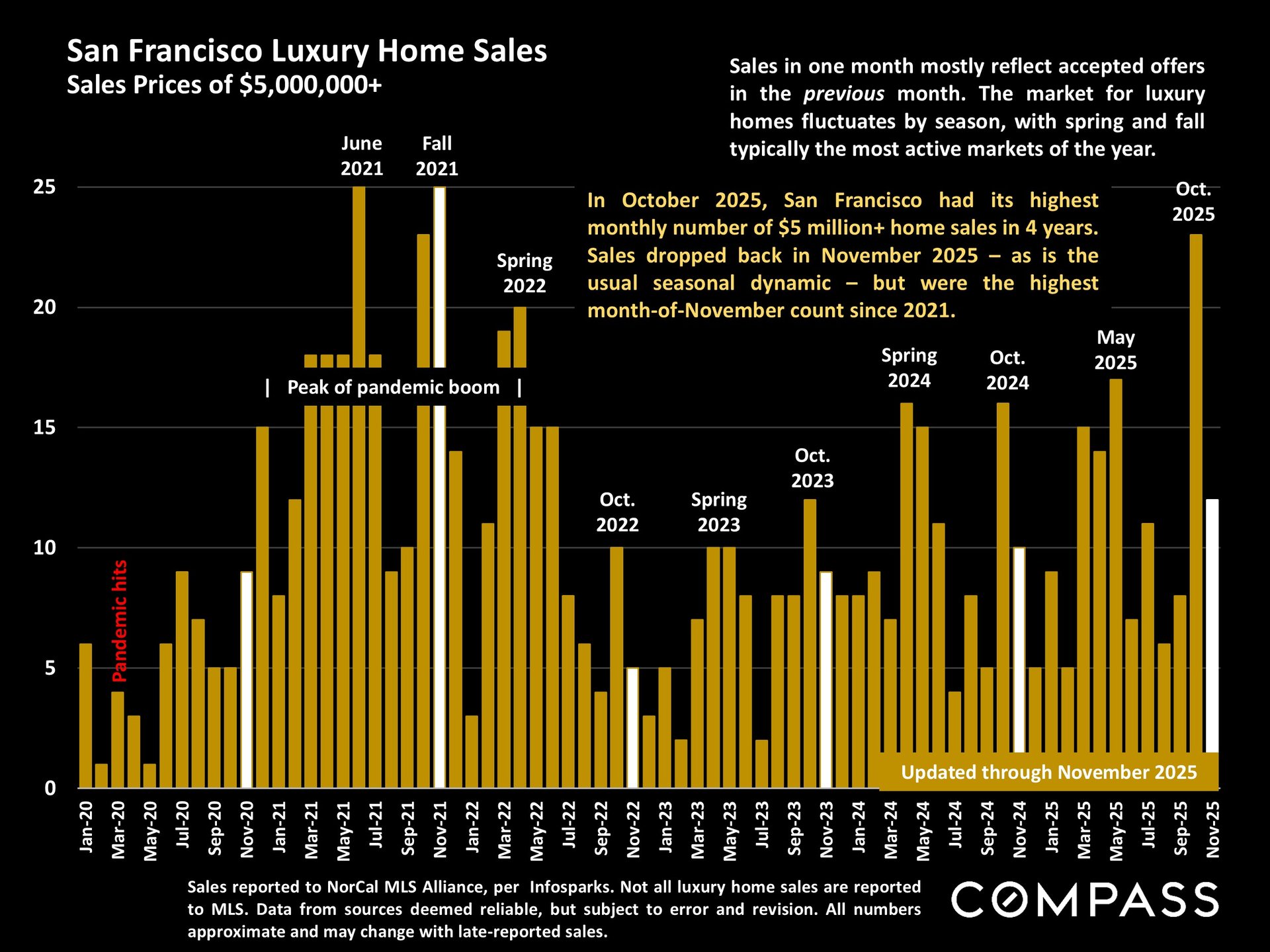

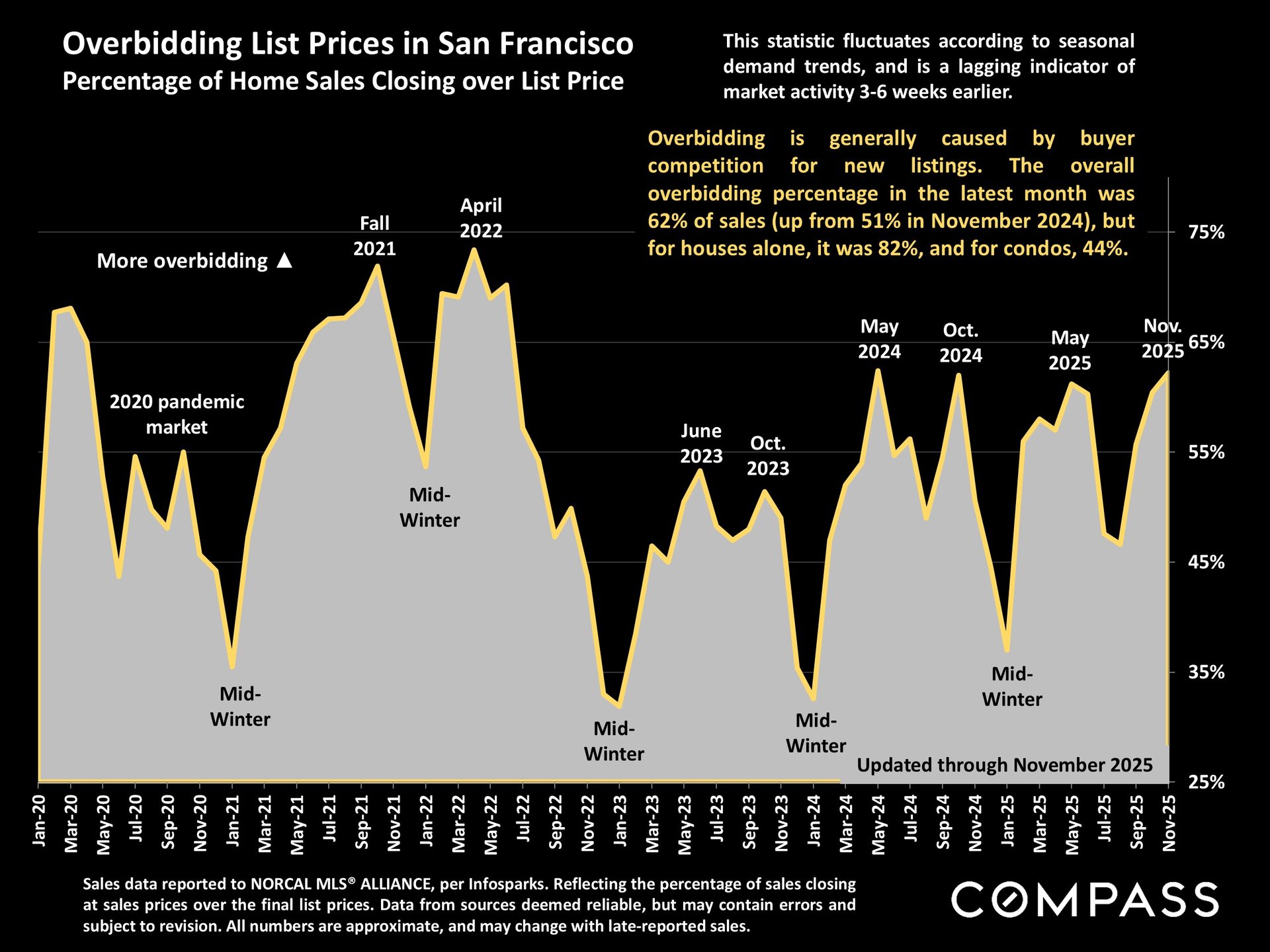

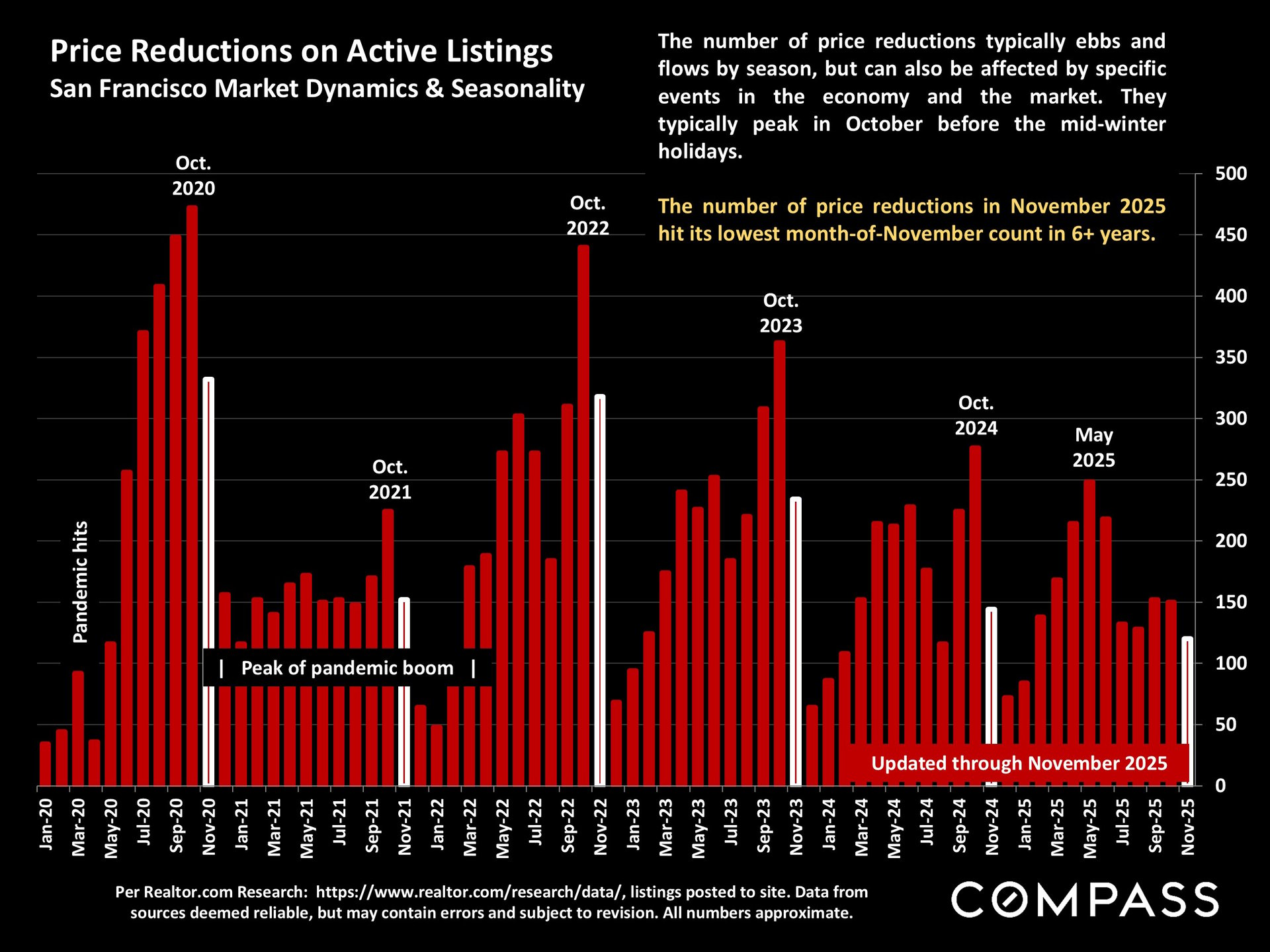

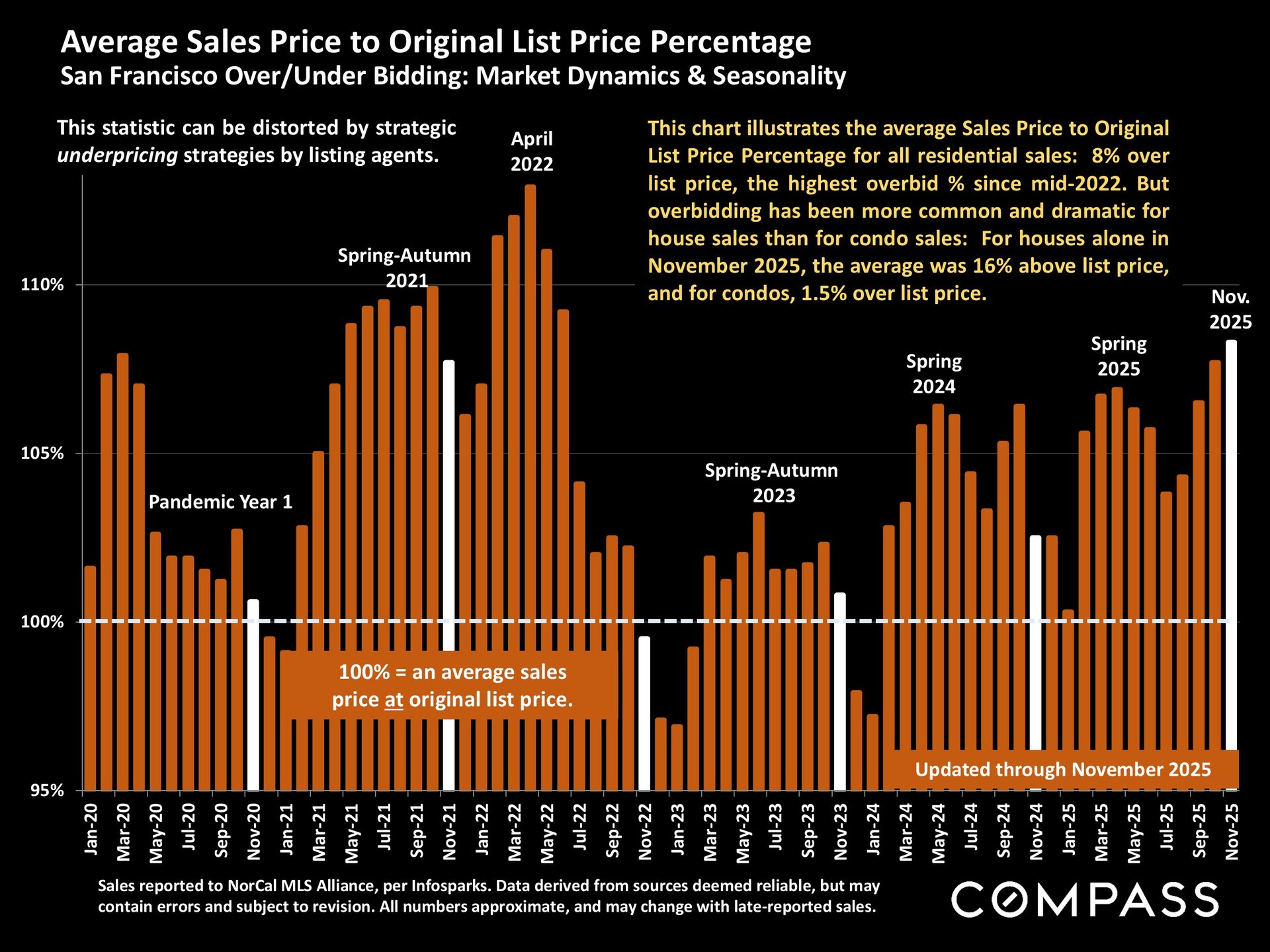

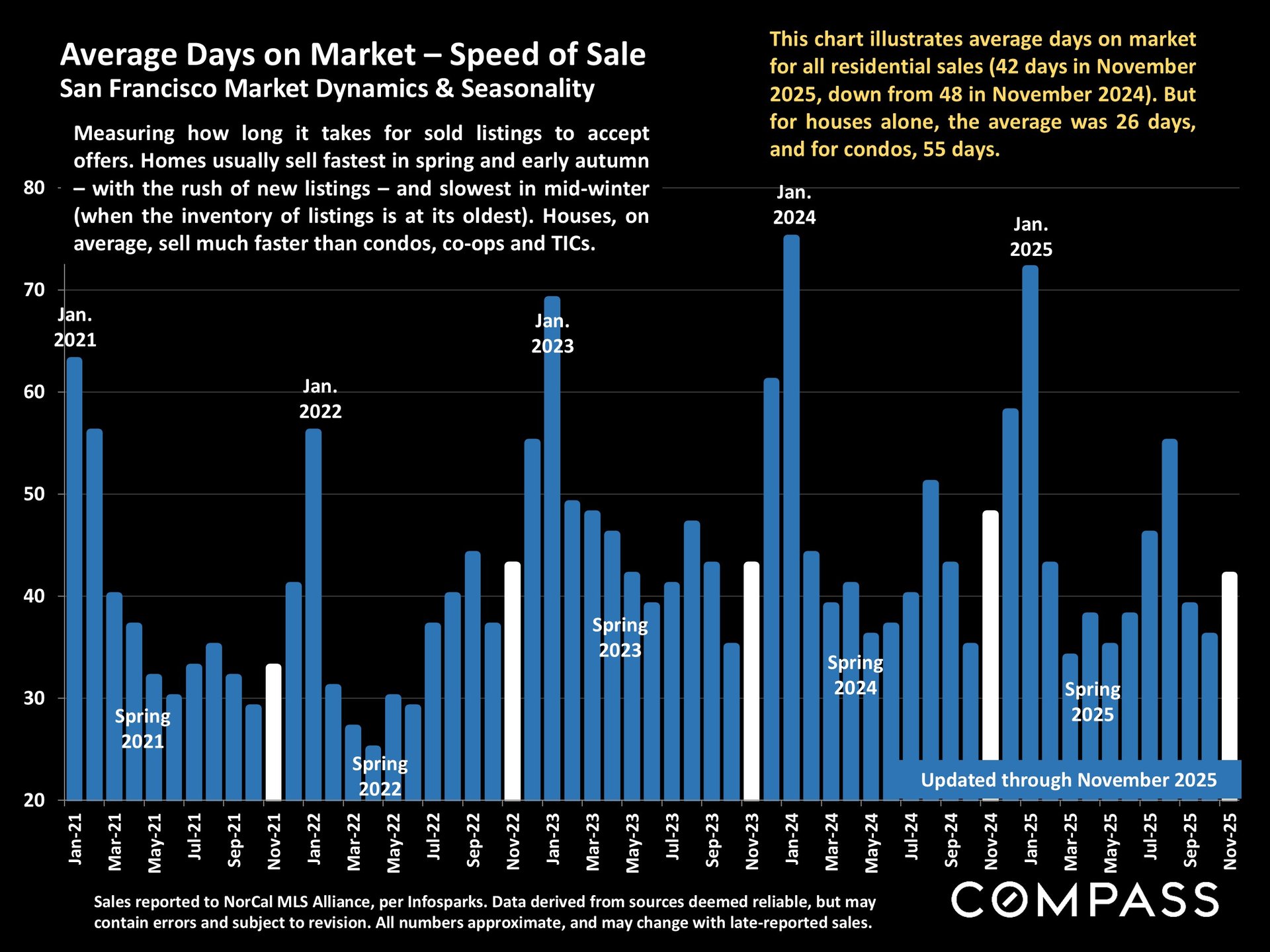

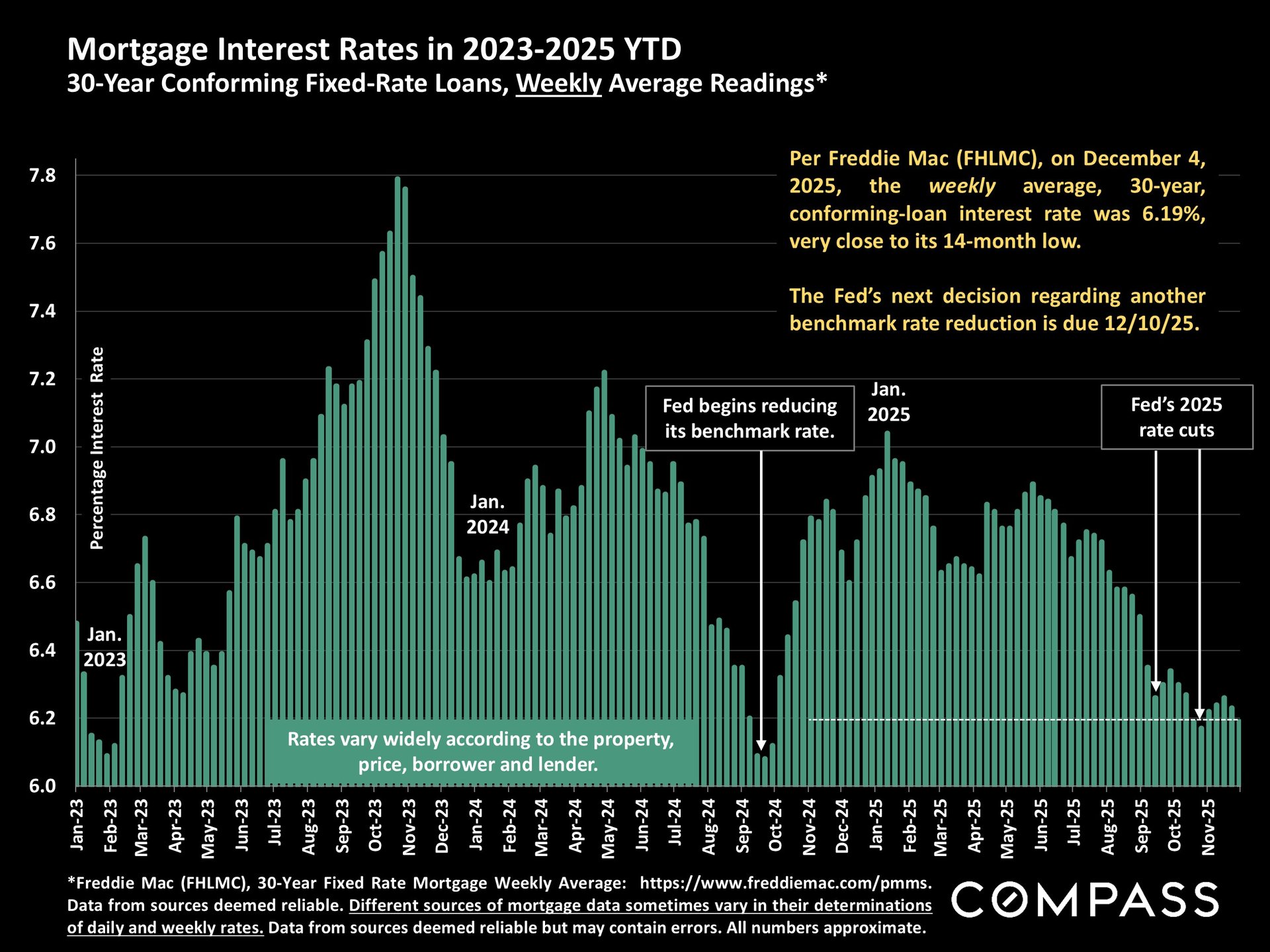

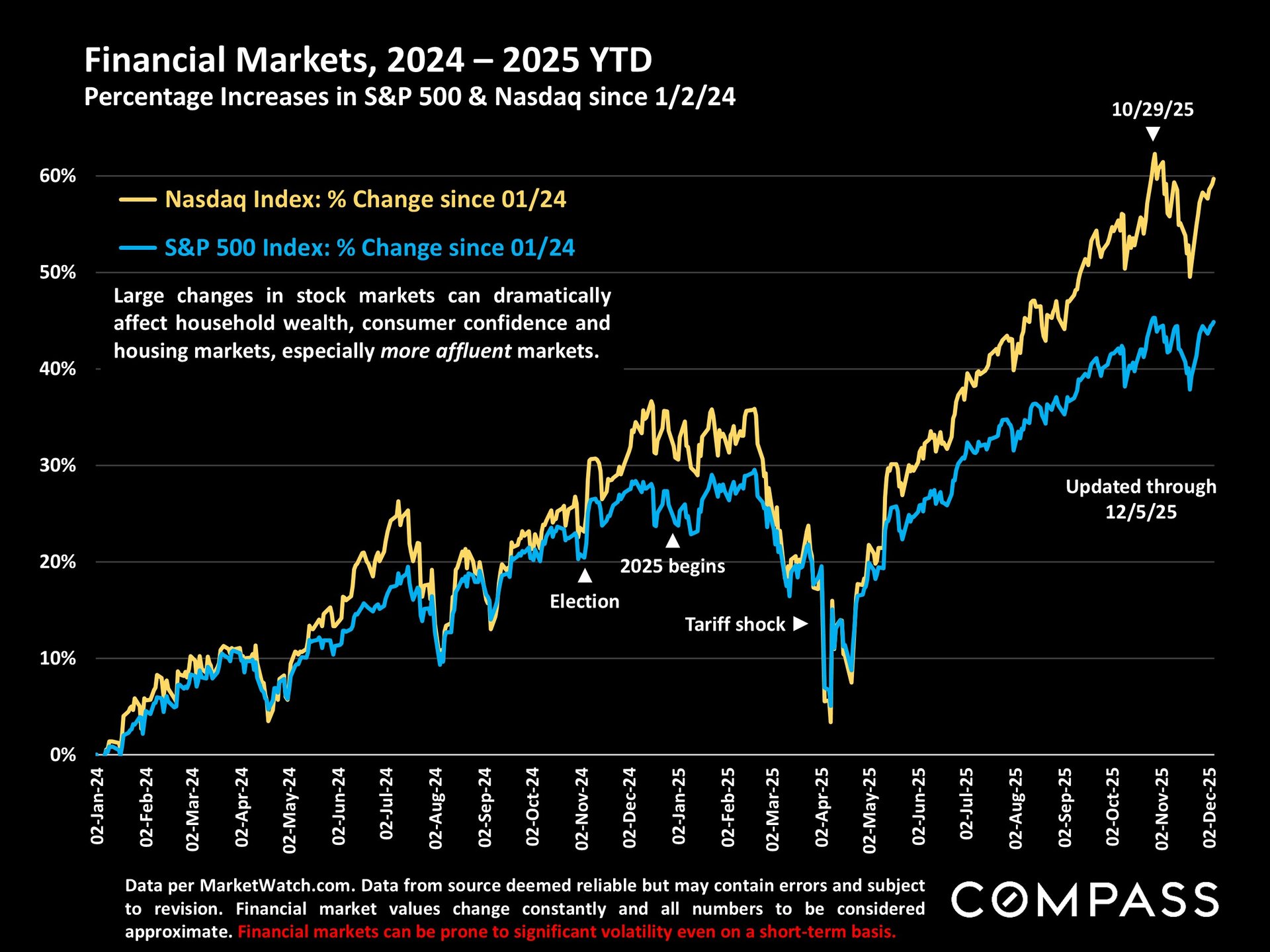

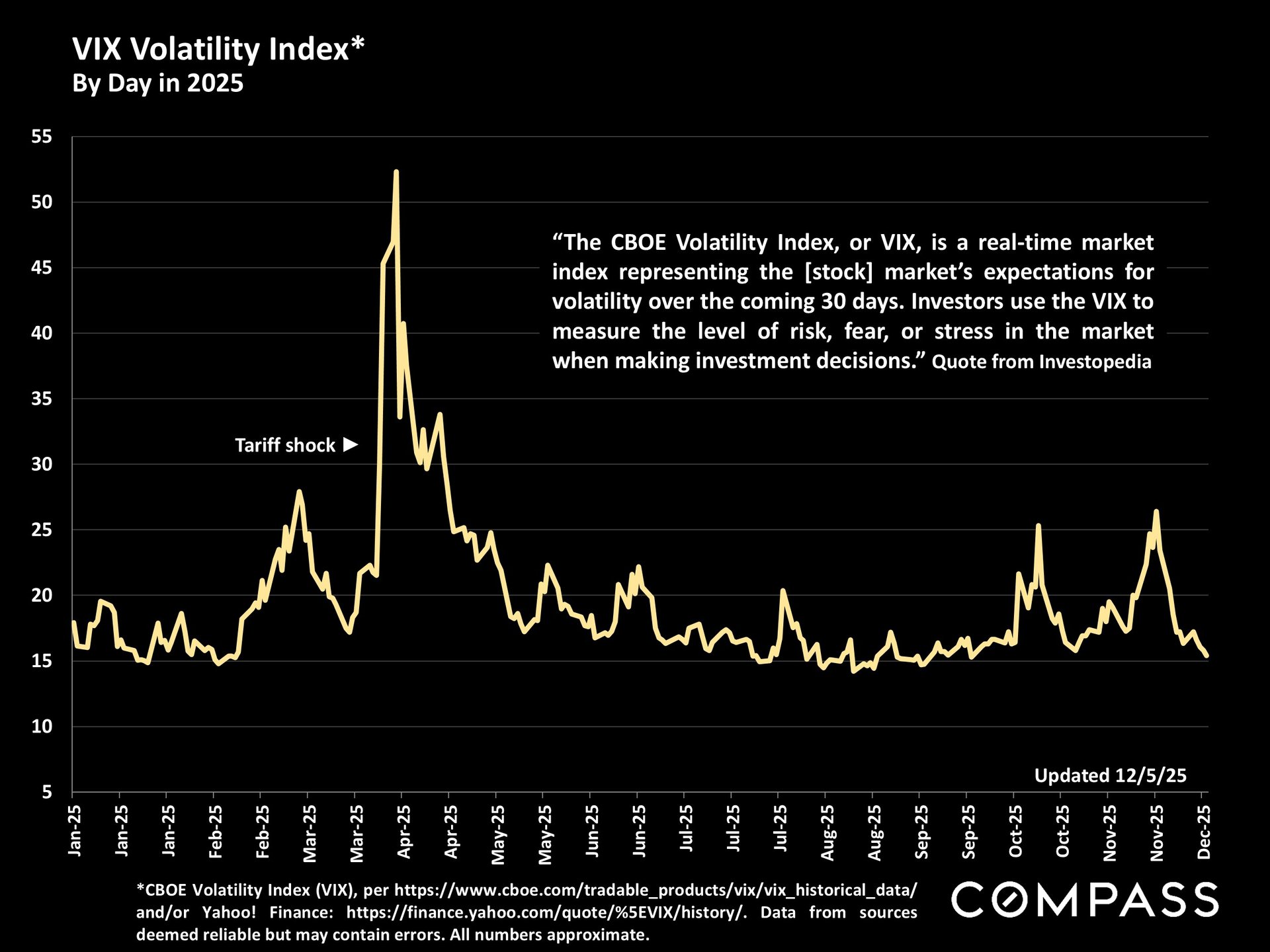

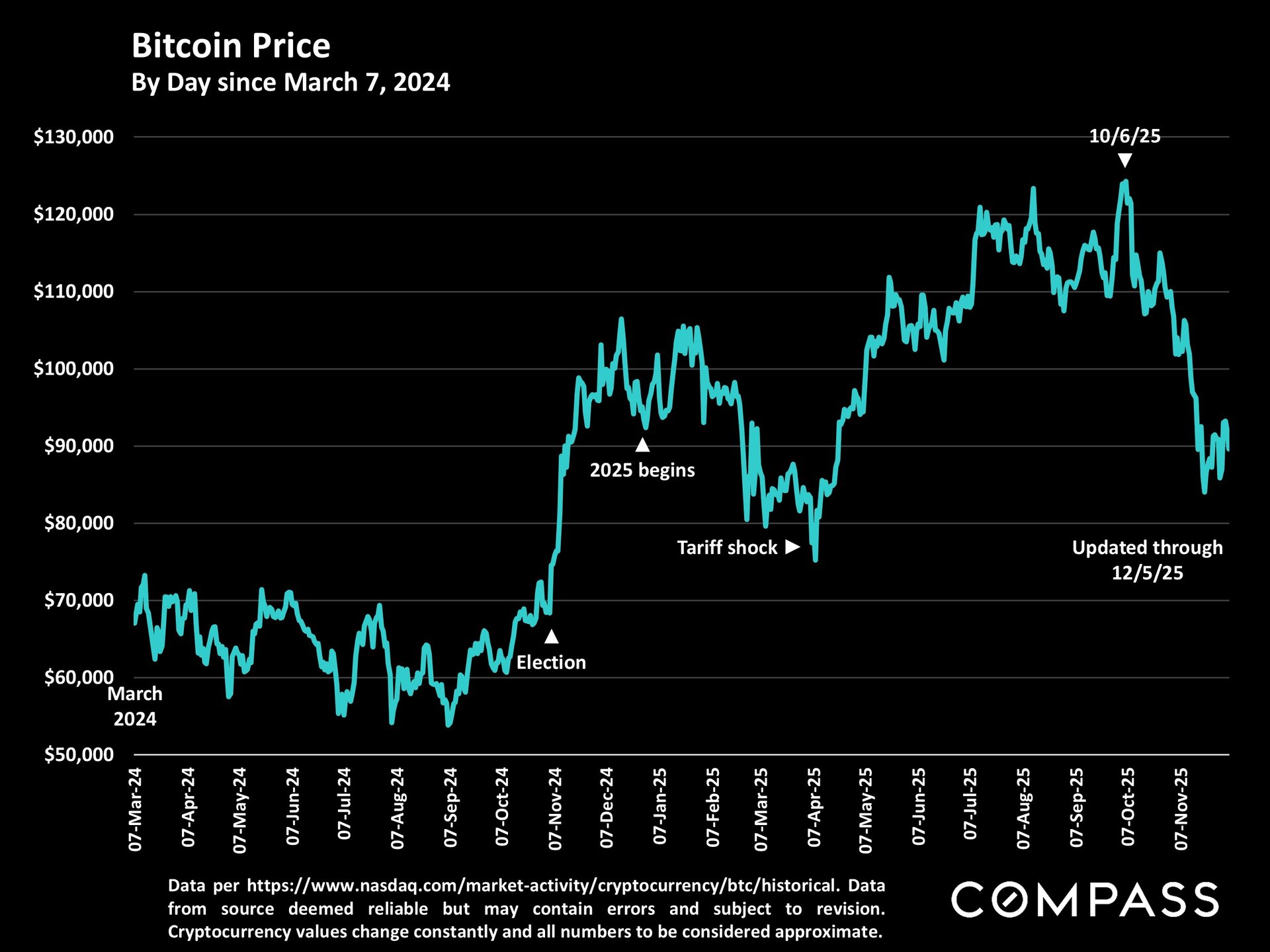

The real estate market entered its typical mid-winter holiday slowdown in November, marked by a notable decline in both listing and sales activity. This seasonal contraction generally accelerates through December—historically the slowest month of the year—before market activity begins to reawaken in mid-January. As illustrated in this report, virtually every indicator—pricing, inventory levels, overbidding, and speed of sale—points to a remarkable surge in demand across San Francisco this past fall. We attribute much of this momentum to the accelerating AI startup boom within the city. As a result, San Francisco now ranks among the most heated real estate markets in the country. Attention now turns to the New Year’s market. Historically, the start of the year has often brought a significant uptick in activity that continues to build through the spring. This pattern emerged in early 2025 before being disrupted by the “tariff shock” and subsequent economic reactions, which triggered a meaningful slowdown beginning in April. In the broader financial landscape, the first week of December saw both the S&P 500 and Nasdaq largely recover from their November declines, while the 30-year mortgage rate hovered near a 14-month low. Although consumer confidence edged up modestly from November, it remains well below long-term averages—yet this appears to have had little impact on San Francisco’s housing market. Market attention is now focused on the Federal Reserve’s upcoming decision regarding a potential year-end benchmark rate reduction, as well as the inflation report scheduled for later this month.

Address

891 Beach Street

San Francisco, CA 94109

Sabrina Gee-Shin | CA DRE# 01457747

Embrace SF Team